26 Apr 2023

1. The Government announced today increases in the Additional Buyer’s Stamp Duty (ABSD) rates to promote a sustainable property market. The revised rates will take effect from 27 April 2023.

2. The implementation of the property market measures in December 2021 and September 2022 have had a moderating effect. However, in 1Q2023, property prices showed renewed signs of acceleration amid resilient demand. Demand from locals purchasing homes for owner-occupation has been especially strong, and there has also been renewed interest from local and foreign investors in our residential property market. If left unchecked, prices could run ahead of economic fundamentals, with the risk of a sustained increase in prices relative to incomes.

Raising Additional Buyer’s Stamp Duty (ABSD) Rates

3. To promote a sustainable property market and prioritise housing for owner-occupation, the Government will raise the ABSD rates further to pre-emptively manage investment demand.

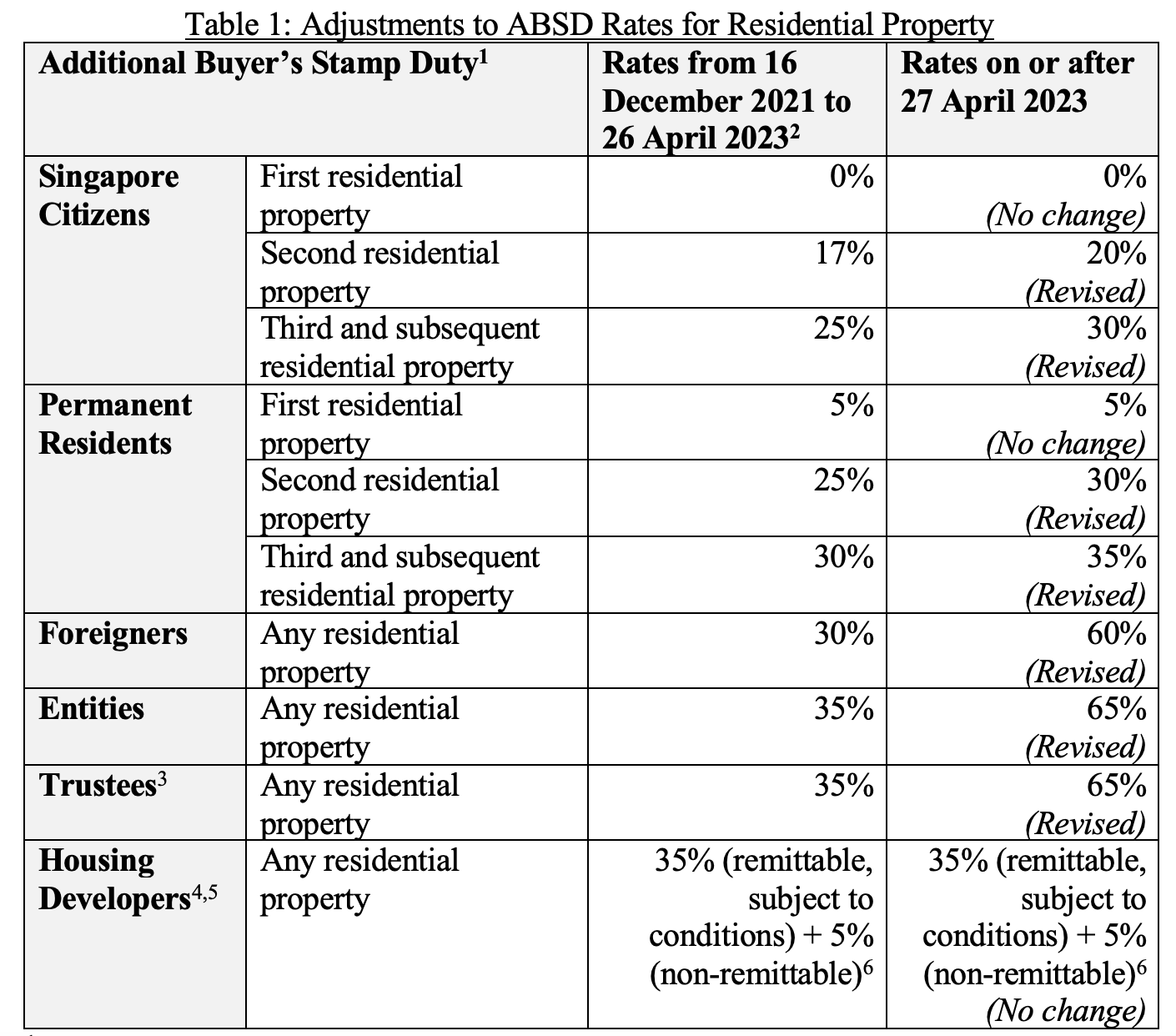

4. The specific ABSD rates increases are as follows:

a. Raise ABSD rate from 17% to 20% for Singapore Citizens (SCs) purchasing their 2nd residential property;

b. Raise ABSD rate from 25% to 30% for SCs purchasing their 3rd and subsequent residential property, and Singapore Permanent Residents (SPRs) purchasing their 2nd residential property;

c. Raise ABSD rate from 30% to 35% for SPRs purchasing their 3rd and subsequent residential property;

d. Raise ABSD rate from 30% to 60% for foreigners purchasing any residential property; and

e. Raise ABSD rate from 35% to 65% for entities or trusts purchasing any residential property, except for housing developers.

5. Based on 2022 data, the above ABSD rate increases will affect about 10% of residential property transactions.

6. The ABSD rates for SCs and SPRs purchasing their first residential property, which constitutes about 90% of residential property transactions based on 2022 data, will remain at 0% and 5% respectively.

7. Table 1 summarises the adjustments to the ABSD rates.

| 1 The ABSD residential property count includes properties that are owned wholly, partially, or jointly with others. 2 The ABSD (Trust) rate was for the period from 9 May 2022 to 26 April 2023.3 ABSD (Trust) is payable by a trustee of any trust when acting in that capacity, but excludes the following: (a) trustee for a collective investment scheme when acting in that capacity; (b) trustee-manager for a business trust when acting in that capacity; (c) trustee for a housing developer when acting in that capacity. (a)/(b) and (c) are already subject to ABSD (Entity) and ABSD (Housing Developer) respectively, when they acquire residential property.4 Housing developers refer to entities in the business of housing development (i.e. construction and sale of housing units) with respect to the subject property acquired. These include trustees for housing developers.5 Housing developers may apply for remission of this ABSD, subject to conditions.6 This 5% will not be remitted and is to be paid upfront upon purchase of residential property. |

8. For acquisitions made jointly by two or more parties of different profiles, the highest applicable ABSD rate will apply.

9. Married couples with at least one SC spouse, who jointly purchase a second residential property, can continue to apply for a refund of ABSD, subject to conditions. These conditions include selling their first residential property within 6 months after (a) the date of purchase of the second residential property if this is a completed property, or (b) the issue date of the Temporary Occupation Permit (TOP) or Certificate of Statutory Completion (CSC) of the second residential property, whichever is earlier, if the second property is not completed at the time of purchase.

10. The ABSD currently does not affect those buying an HDB flat or Executive Condominium unit from housing developers with an upfront remission, if any of the joint acquirers/purchasers is a SC. There will be no change to this policy.

11. The revised ABSD rates will apply to all residential properties acquired on or after 27 April 2023. There will be a transitional provision, where the ABSD rates on or before 26 April 2023 will apply for cases that meet all the conditions below:

a. The Option to Purchase (OTP) was granted by sellers to potential buyers on or before 26 April 2023;

b. This OTP is exercised on or before 17 May 2023, or within the OTP validity period, whichever is earlier; and

c. This OTP has not been varied on or after 27 April 2023.

12. Correspondingly, the Additional Conveyance Duties for Buyers (ACDB), which applies to qualifying acquisitions of equity interest in property holding entities (PHEs)1 will be raised from up to 46% to up to 71%.

Significant Increases in Housing Supply

13. The revisions to the ABSD rates to help moderate investment demand will complement our efforts to ramp up supply, to alleviate the tight housing market for both owner-occupation and rental.

14. We have increased the supply of private housing on the Confirmed List to 4,100 units for the 1H2023 Government Land Sales (GLS) programme, from 3,500 units for 2H2022. In 2022, we had injected a total of 6,300 units under the Confirmed List. For public housing, we have launched more than 23,000 flats in 2022 and will launch up to 23,000 flats in 2023. We are also prepared to launch up to 100,000 new flats in total between 2021 to 2025. We will continue to maintain a steady pipeline, to cater to growing housing demand.

15. While COVID-19 had led to severe delays across private and public housing projects, we have made good progress to get back on track. With almost 40,000 public and private residential property completions in 2023, and near 100,000 units expected to be completed from 2023 to 2025, there will be significant housing supply coming onstream over the next few years.

16. The measures above have been calibrated to moderate housing demand while prioritising owner-occupation, and provide sufficient housing supply. The Government will continue to adjust our policies as necessary to ensure that they remain relevant, and promote a sustainable property market.

Issued by:

Ministry of Finance, Ministry of National Development and Monetary Authority of Singapore

1A PHE is an entity which has at least 50% (i.e., asset ratio) of its total tangible assets comprising prescribed immovable properties in Singapore. Please refer to IRAS’ website for more details on PHEs and prescribed immovable properties.

Source: MOF | Press Releases